Northam receives positive credit rating amid improving operational profile

Credit rating agency GCR Ratings has revised the outlook on JSE-listed Northam Platinum’s long-term issuer rating to positive, on the back of an improving operational profile, expected stronger earnings and financial position.

Northam says GCR has affirmed its national scale long-term and short-term issuer ratings at A+(ZA) and A1(ZA), respectively, with the rating outlook revised to positive from stable.

Concurrently, GCR has affirmed parent company Northam Platinum Holdings' national scale long-term and short-term issuer ratings at A+(ZA) and A1(ZA), respectively. The rating outlook has been revised to positive from stable.

Northam says the affirmation of its rating and the revision of its outlook to positive reflect the continued operational development at the group's mines, which together with its sustainable cost advantage, serve to enhance its business profile.

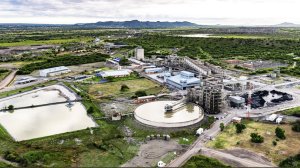

Northam notes that it has reached sales of one-million ounces of platinum, palladium, rhodium and gold (4E) platinum group metals (PGMs) and is nearing its one-million-ounce production target from own operations – excluding bought metal.

With PGM prices having notably improved and forecast to remain broadly firmer, GCR anticipates upside to its base case and expects earnings to improve significantly and gearing metrics to strengthen.

Additionally, Northam is expected to maintain a robust liquidity profile.

GCR notes that Northam's competitive position has progressively strengthened through strong project execution, leading to continued production expansion and the prioritisation of operational improvements.

Northam says GCR views the company’s low-cost position as a key benefit to through-the-cycle profitability.

Additionally, chrome production has also become a valuable emerging businesses segment, serving to diversify income streams.

Northam notes that it has advanced its environmental strategy, including various large-scale renewables projects at different stages of completion, which will strengthen energy security, lower long-term energy costs and enable it to achieve its decarbonisation targets.

It says the positive outlook reflects GCR's view that sustained operational improvements, disciplined capital management and the expected earnings recovery will strengthen Northam's credit profile over the next 12 to 18 months.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

Virtual Gas Network supplies compressed natural gas via a virtual gas distribution network.

VISIT SHOWROOM

For over 15 years, Lilak Aluminium, a trusted leader in architectural extrusion supply, has delivered excellence to businesses like yours.

VISIT SHOWROOM

Press Office

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation