Investment decision end June on already well-infrastructured Burnstone gold project

Sibanye-Stillwater COO South Africa Richard Cox.

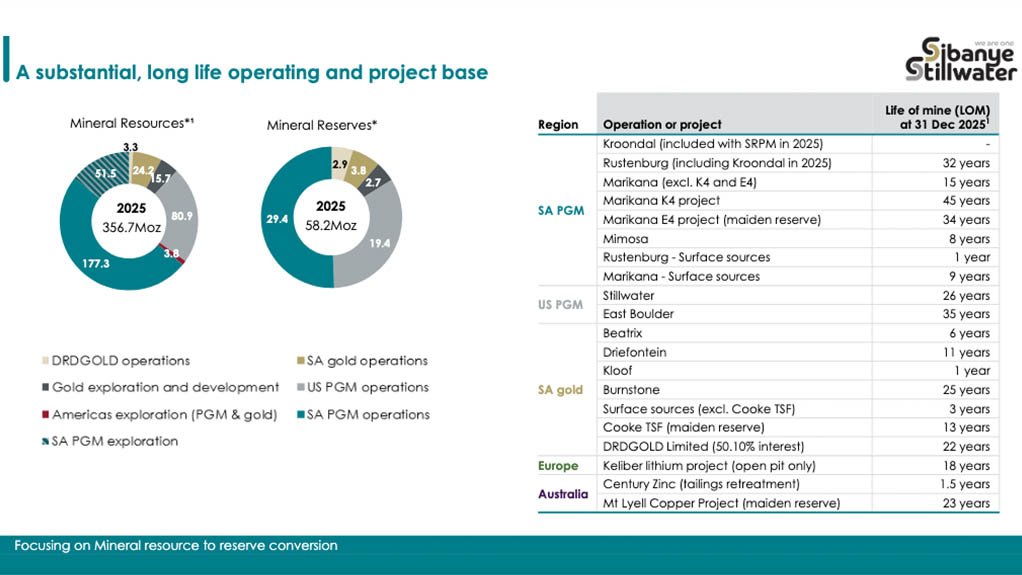

The lives of Sibanye-Stillwater assets.

JOHANNESBURG (miningweekly.com) – The final investment decision by Sibanye-Stillwater on the already well-infrastructured Burnstone gold project in South Africa’s Mpumalanga province is being targeted for the first half of this year.

At the same time, the strong foundation being created by Sibanye-Stillwater on the platinum group metals (PGMs) front is enabling the Johannesburg Stock Exchange-listed precious metals company to capitalise on the considerably stronger PGM prices.

"With supported fundamentals, potential for additional earnings and cash flow improvements in 2026 is anticipated, allowing continued investing through the cycle in low-risk, low-capital intensity projects with quick paybacks, all supporting stable, high performing operations with optionality to extend our portfolio," is the comment that paints the overall picture amid advantage being taken of substantial project capital having already been expended at the 25-year life-of-mine Burnstone project, where underground infrastructure is in place and surface infrastructure is mostly done. All this has been taking place near the town of Balfour, about 80 km south-east of Johannesburg, in the Dipaleseng municipality.

“The plant’s largely built,” Sibanye-Stillwater CEO Richard Stewart reported in response to RMB Morgan Stanley research and equity head analyst Chris Nicholson's capital expenditure questioning at last week’s comprehensive presentation covered by Mining Weekly.

The remaining capital required is predominantly to open up the orebody. “What we’re really looking at is the cost of going from start up to steady state,” Stewart explained.

Meanwhile the feasibility under way exemplifies Sibanye-Stillwater’s one-million-reserve-ounce strategic shift to a higher-margin, shallower gold-mining focus that extends beyond Burnstone to Cooke surface gold, located about 35 km south-west of Johannesburg near the town of Randfontein; Beatrix gold operations, near Welkom and Virginia in the Free State; and attributable surface gold from DRDGOLD, 50 km east of Johannesburg in Brakpan and 80 km west of Johannesburg in Carletonville.

On top of all that, Sibanye-Stillwater’s many mature gold operations – also see attached infographic – are highly geared to gold prices and are already generating strong cash flows in the current highly supportive price environment.

“Looking forward, our core gold operations will continue to drive performance excellence, and we are excited about the prospects in our current portfolio,” Sibanye-Stillwater COO South Africa Richard Cox enthused.

For 2026, the outlook is positive. Spot prices are up 9% year-to-date to over R2.5-million/kg and 20% above second half 2025 levels, all boding well for another successful year with potential earnings and cash flow growth.

How rising prices are opening up expanding margins was illustrated on a gearing and all-in sustaining cost (AISC) margin chart, which showed the average gold price received climbing steadily against controlled AISC.

In addition, a free cash flow bar chart highlighted the magnitude of the rapid cash flow turnaround, moving from negative in 2024 to significantly positive in 2025.

However, total production, including DRDGOLD, was 10% down. Underground production fell by 8% on operational challenges at Kloof and surface production was down 16% – an impact mitigated by a 39% gold price boost.

The AISC increased 15% to R1.4 million/kg, with 14% lower gold sold.

Persistent 2025 Kloof challenges included a shaft incident at Manyano 7 Shaft, aging ventilation pass infrastructure and ore-pass systems, logistics constraints, as well as seismic risk in high-grade isolated blocks of ground (IBGs).

The resulting 31%-lower year-on-year 2025 production to 3 374 kg prompted a rebasing of the plan and a life-of-mine adjustment to one year, amid safety being the number-one priority.

Several Kloof teams were consequently relocated from higher-risk IBGs to Sibanye-Stillwater’s Driefontein gold operations.

Subsequently, after a review process, Kloof’s higher-risk IBGs were torn from the long-term plan, to align with risk tolerance.

That said, the sustained rise in the rand gold price over the period boosted adjusted earnings before interest. taxes, depreciation and amortisation (Ebitda) by 115% to R12.5-billion, which represented 33% of group Ebitda and surpassed 2020s record.

Excluding DRDGOLD, Ebitda increased 111% to R6.1-billion on the average price of R1.8-million/kg for the whole gold business.

“We’re pleased to have concluded a three-year wage agreement with labour, which provides a degree of cost certainty moving forward. There is a lot of work underway supporting our strategic transitioning of the gold business, and this effort is to ensure long-term sustainability.

Questioned by SBG Securities executive director and research analyst Adrian Hammond about how Kloof’s closure liabilities differed from those of Cooke’s R1-billion-a-year pumping costs, Stewart said pumping issues and liabilities previously experienced at the Cooke shaft were not applicable to either Kloof or Beatrix, but would, in time, become applicable to Driefontein, "and I think that's where there's an important conversation around extending the life of mines around Driefontein, which still has ten years of life ahead of it.”

PLATINUM GROUP METALS

Sibanye-Stillwater’s South Africa PGM operations maintained their consistent delivery, with guidance either being met or exceeded each year since 2017.

“Overall, our South Africa PGM operations are very well positioned to benefit long term and also on the current market upside,” Cox reported.

In 2025, total four-element (4E) PGM production reached 1.8-million ounces, which was in alignment with 1.75-million- to 1.85-million-ounce guidance and stable year-on-year.

Illustrated by a displayed infographic was advancement on the PGM cost curve based upon end-December 2025 data, highlighting its positioning relative to peers.

Marikana’s total cost, including capital expenditure, has been influenced by K4’s project build-up phase.

But as K4 approaches steady state, a shift towards lower costs is being seen. This combined Rustenburg and Kroondal position has moved slightly higher dowing to the Kroondal transition to toll treatment. While this does introduce processing costs, it also enhances profitability through improved revenue and margins.

“Our low capital intensity brownfield projects are poised to further strengthen competitiveness against peers, spot 4E and 6E which includes base metal basket prices, are positioned well above our costs, underscoring our leverage in the prevailing market.

“Our progression from the fourth to the second cost quartile reflects the value of our strategic investments in building long-term sustainable advantage in this business,” Cox pointed out.

Since Sibanye-Stillwater acquired Lonmin in 2019, PGM production has remained steady at between 1.73-million and 1.83-million ounces a year.

Breaking it down, underground production increased by 2% to more than 1.6-million ounces, supported by improvements at Rustenburg’s mechanised Bathopele shaft as well as more stable output at the Siphumelele and Kroondal operations.

At Marikana, output affected by safety-related stoppages at the high-performing Saffy shaft was partially offset by K4’s ramp-up, where production rose 41% to nearly 100 000 oz, which contributed to Marikana's improved cost position.

Surface production was 29% lower at 108 000 oz, influenced by high rainfall and the commencement to transition feed resources such as Rustenburg's Waterval West tailings storage facility as well as two Marikana tailings facilities.

“We’re evaluating long-term surface opportunities at Rustenburg to support the sustainability of the surface business,” Cox reported.

The purchase of concentrate volumes were reduced by 24% in line with contractual terms.

“We remain focused on cost discipline. Operating costs increased by just 7.3% in absolute terms,” Cox pointed out.

AISC rose 10% to just over R24 000/4E ounce and bolstered by byproduct credits of R11.1-billion, was within the guided R23 500/oz to R24 500/oz range.

Stronger ruthenium and iridium contributions helped to offset the 261% increase in royalties to R765-million from higher prices and a 12% rise in sustaining capital to R2.9-billion for key mining equipment and precious metal refinery infrastructure.

Project capital was 16% lower at R675-million owing to completed Rustenburg initiatives and deferred Marikana expenditures and total capex came in at R5.9-billion, which was also under the R6.5-billion estimate.

“The foundation we are creating enables us to capitalise on stronger PGM prices,” said Cox.

The 2025 average 4E basket price increased by 28% to more than R31 000/oz, driving up adjusted Ebitda by 125% to R16.7-billion.

Early 2026 prices have risen 43% to more than R44 000/oz, following an even higher and brief January adjustment.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Projects

Latest Multimedia

Latest News

Showroom

ALBIS FLANGES — founded in 1965 — is a petro-chemical approved manufacturer of flanges and fittings in most grades of steel, listed with Sasol,...

VISIT SHOWROOM

We at Hawk High Pressure Pumps specialise in industrial pumps and pumping systems. Our high pressure washing equipment is locally manufactured and...

VISIT SHOWROOM

Press Office

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation